Hello and happy Fed Meeting Day. Here is a review of the meeting and other news from the previous month in the mortgage world.

National Averages remain in the high-6s (6.85%) for a 30 year conventional loan, down slightly from a month ago.

Fed Meeting:

The Federal Reserve decided to hold the federal funds rate steady again at 4.25–4.50%. They penciled in two rate cuts later this year, while trimming expectations for fewer cuts in 2026. The updated "dot plot" reflected tempered economic forecasts, with 2025 GDP growth revised down to 1.4% and the unemployment rate up to 4.5%. Inflation was projected to gradually move toward 3% by year-end, and Powell continues to say rates will stay at their level until inflation comes down. Trump has continued to call Powell a "numbskull" and today added "Am I allowed to appoint myself at the Fed? I’d do a much better job than these people." Powell's term ends in 2026 and we can expect someone else to take the reins, likely someone more aligned with Trump's vision for lower interest rates.

Inflation & Job Data:

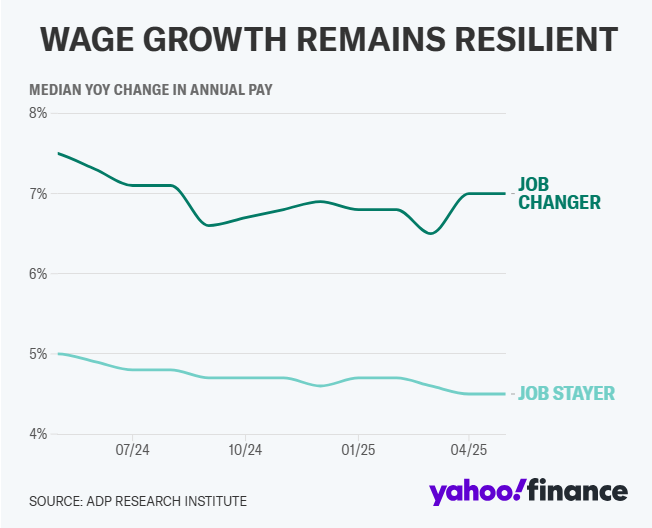

The drop in mortgage rates starting on June 6th came on the back of soft inflation data. The May CPI releases came in at 2.4% (YoY) and Core CPI at 2.8%. This led to a roughly 10-basis-point drop in the 10‑year Treasury yield. Meanwhile, labor-market indicators showed potential cracks as weekly jobless claims rose to about 248,000. Rising jobless claims show the difficulty to get a new job right now. If you can find one though, the data shows you are rewarded with a much higher increase in salary than staying pat.

Geopolitical news:

Geopolitical tensions surged after an Israeli airstrike on Iran, driving oil prices up by 13% as markets braced for supply disruptions and regional instability. This spike in oil costs added a layer of complexity to the inflation outlook just as price pressures were beginning to ease (partially due to lower gas prices). At the same time, U.S.–China trade relations showed signs of improving, with early discussions suggesting the relaxing of some export tariffs. Most other existing tariffs remain at a 10% baseline but those pauses will end on July 9th. Together, these crosscurrents showcase the fragile balance facing global relations and the effected markets.

Consumer Confidence:

The May dataset for consumer confidence rebounded sharply, up 16% from April. Digging into the data, many individuals cited a pause in US-China Tariffs to help boost their economic confidence. We're still down 20% from December levels, but this is a good sign for the Housing Market as improving consumer confidence is a great indicator of an increase in buyers.

Some Local Stories:

Broncos Stadium

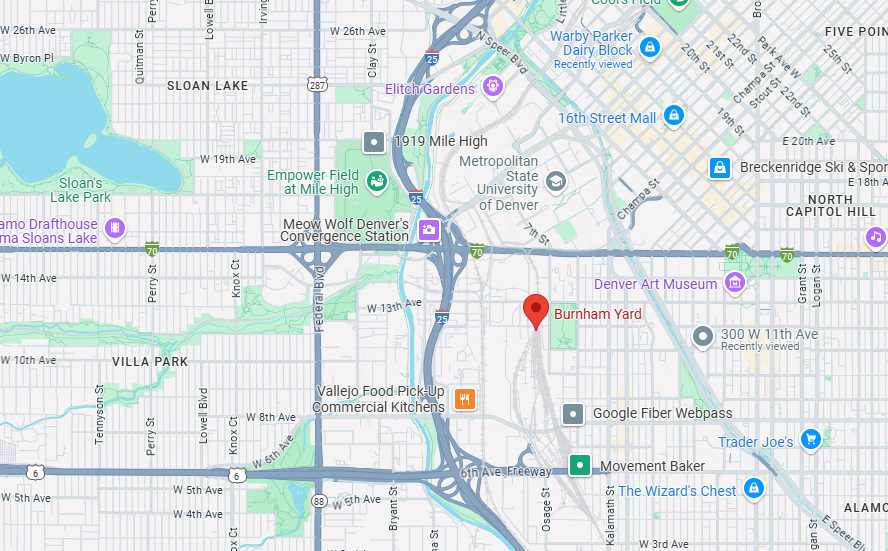

The Broncos bought $146 million in land in Burnham Yard in the last few months (6th and i25 is your closest major intersection). Here's a map since I know you want one. The team's lease at the current stadium ends in 2031 and there is a lot of hype surrounding where they'll play after that. Predicting that, and buying nearby real estate, could be a worthwhile investment. Read more here.

Pools?

Axios/Realtor.com are reporting 24.9% of Denver listings have pools. That seems CRAZY high to me and I'm guessing has to be driven higher by condos. This was a fun article to read, especially because two of the houses are within a half mile of my house, so naturally I checked them out. Maybe it's because I have a toddler and my parent-spidey-senses were going off but I was not a fan.